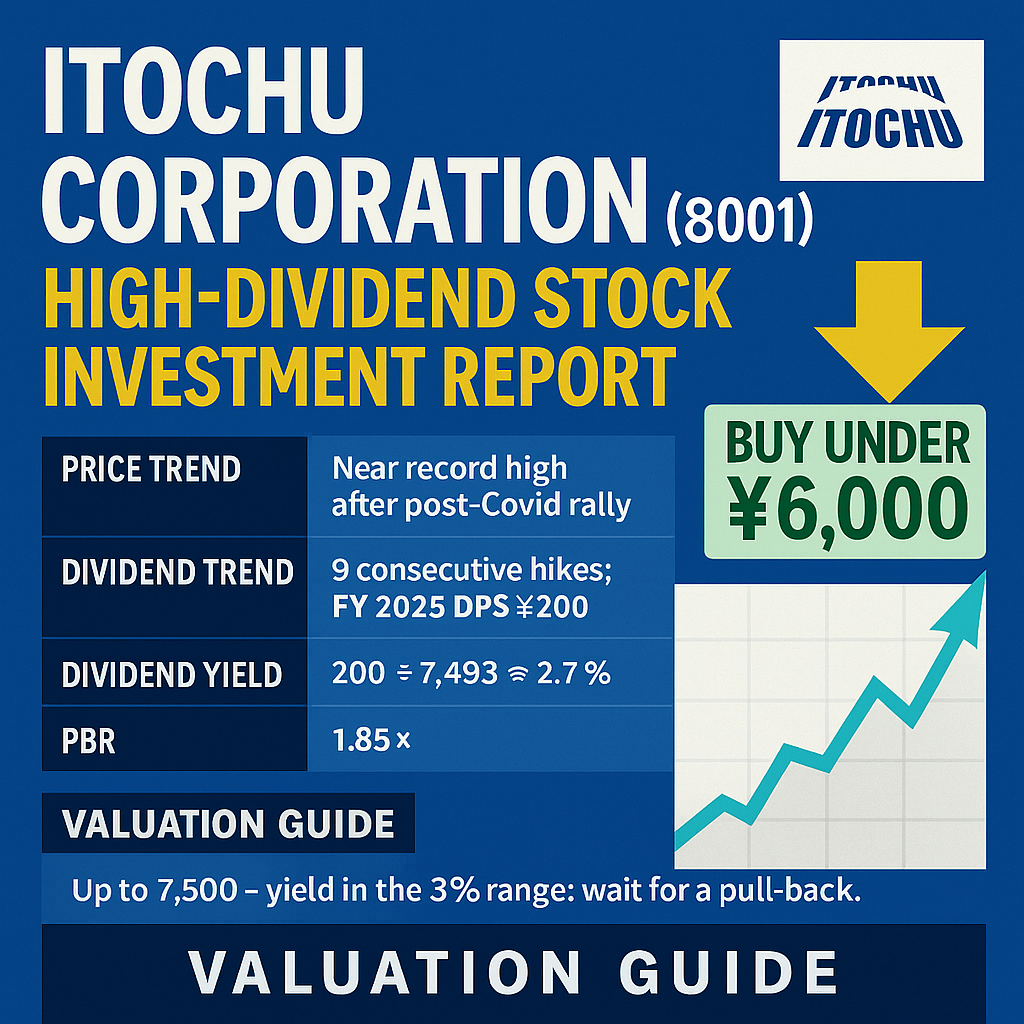

Itochu (8001): Why Buffett Loves this "Non-Resource" King (And You Should Too)

s7たち

Best Japan Stocks

A Mega-Bank–Backed Ultra-Stable Dividend Compounder in Japan

Fuyo General Lease is one of Japan’s leading comprehensive leasing companies.

The company provides long-term leasing and installment sales financing for:

In Japan, leasing companies are not merely “rental businesses.” They function as part of the country’s financial infrastructure, supporting long-term corporate capital investment in a role similar to that of commercial banks.

Fuyo General Lease is regarded as one of Japan’s “Big Three Leasing Companies,” alongside ORIX and Mizuho Leasing, forming the core of Japan’s highly stable leasing industry.

Fuyo General Lease is affiliated with Sumitomo Mitsui Financial Group (SMFG), one of Japan’s top three mega-banking groups.

SMFG is a global financial institution that operates:

across Japan, Asia, Europe, and the United States. It is recognized as one of the most creditworthy financial groups in Japan.

Thanks to this backing, Fuyo General Lease benefits from:

This mega-bank support significantly enhances the company’s financial safety and long-term dividend sustainability.

In Japan, major leasing companies play a vital role in financing:

These sectors remain essential even during economic downturns, making demand for leasing highly resilient.

As a result, Japan’s leasing industry is characterized by:

Fuyo General Lease has long been a core player within this exceptionally stable financial ecosystem.

Most of Fuyo General Lease’s revenue is generated through long-term lease contracts lasting approximately 3 to 7 years.

This model offers several powerful advantages:

Over roughly the past decade:

This demonstrates high-quality growth in both scale and profitability.

Its client base is also well diversified across:

which significantly reduces dependence on any single industry.

Because leasing companies must purchase assets upfront and recover them over several years, operating cash flow is structurally negative.

This is not a warning sign of financial distress. Instead, for Fuyo General Lease, negative operating cash flow reflects:

The company’s equity ratio has improved from roughly 10% to the low-13% range over the long term, indicating a steady strengthening of its financial base.

Supported by SMFG, Fuyo General Lease maintains:

As a result, liquidity risk remains extremely low even in rising interest-rate environments.

One of the company’s greatest attractions is its 15 consecutive years of dividend increases.

Recent dividend conditions are approximately:

The payout ratio is maintained in the 30–35% range, allowing:

Management explicitly states that its basic policy is to deliver “stable and continuous dividend increases.”

This clearly reflects a long-term shareholder-oriented capital allocation philosophy rather than short-term profit maximization.

Key valuation metrics are currently around:

Compared with peers such as Mizuho Leasing and ORIX, Fuyo General Lease trades in the attractive value zone for income-oriented investors.

Assuming a target yield of 4.0%, a share price of 10,000 JPY or below would represent an especially compelling long-term entry point.

Despite its stability, several risks should be recognized:

However, these risks are mitigated by:

Therefore, the probability of sudden structural deterioration remains low.

Fuyo General Lease represents:

This stock is not intended for short-term trading. Instead, it is ideally suited for investors seeking:

For global investors looking to build a low-volatility, income-focused Japan equity portfolio, Fuyo General Lease stands out as one of the most reliable candidates.

The content on this website is for informational and educational purposes only and does not constitute financial, legal, or investment advice. The views expressed are the personal opinions of the author (DividendDan), based on experience as a strategy consultant and individual investor living in Japan.

Market data and company information are subject to change. Please conduct your own due diligence or consult a certified financial advisor before making any investment decisions. The author may hold positions in the securities mentioned.