Escaping US Regional Bank Risks? Why Japan's Mega-Bank "MUFG (8306)" Has Just Entered Its Golden Age

s7たち

Best Japan Stocks

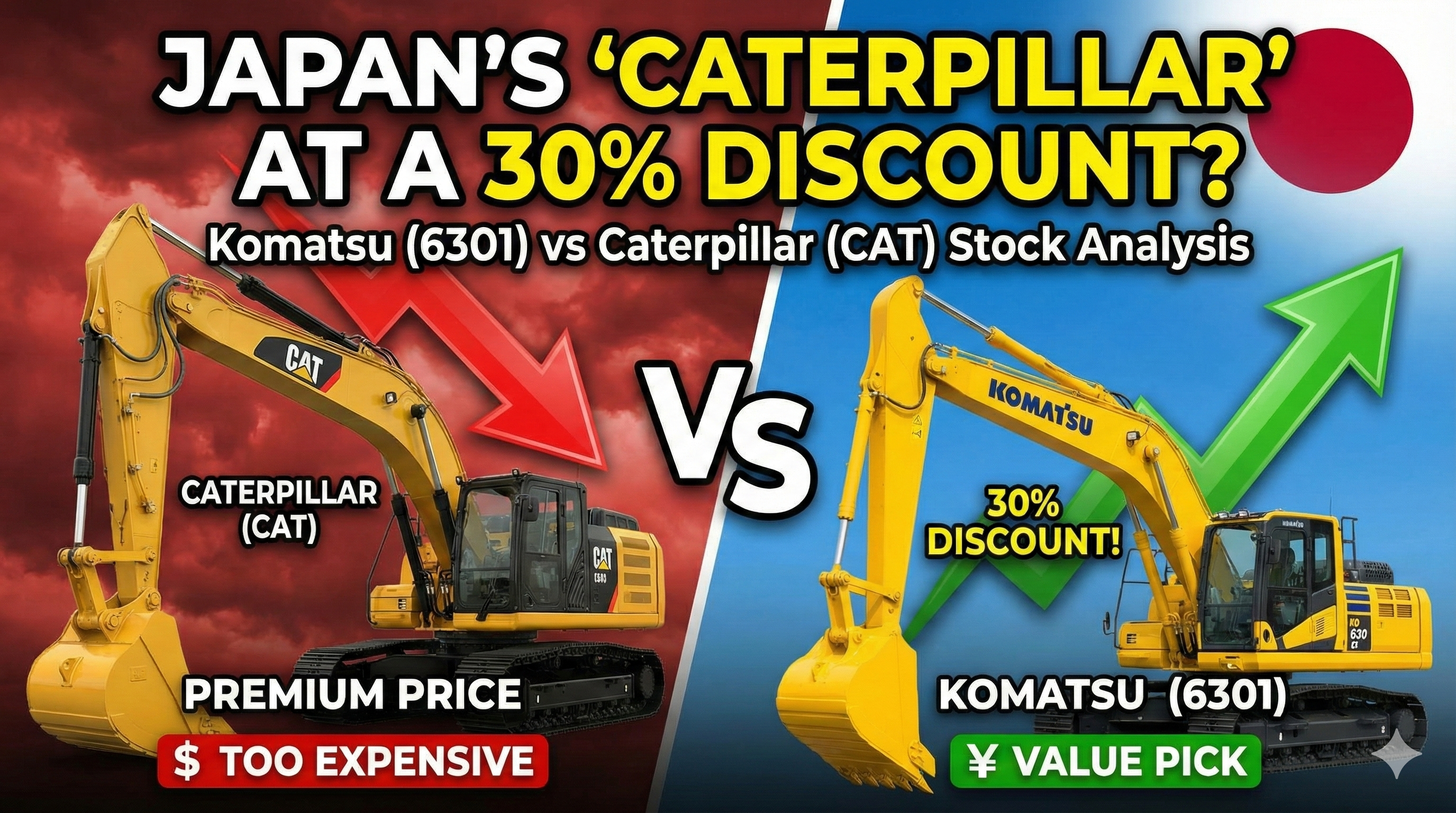

- ✅ The “Caterpillar” of Japan: Komatsu is the world’s second-largest construction equipment manufacturer, right behind Caterpillar (CAT).

- ✅ Massive Valuation Gap: While CAT trades at a premium valuation (P/E ~14-18x), Komatsu is often available at a significant discount (P/E ~10-12x).

- ✅ Weak Yen Benefit: With over 80% of sales coming from outside Japan, Komatsu is a major beneficiary of the strong Dollar / weak Yen.

If you are an industrial investor, you probably have Caterpillar (CAT) on your watchlist. It is the undisputed king of “Yellow Iron.” But there is one problem: Everyone knows it. Because CAT is so popular, its stock price often carries a “premium” price tag.

But what if you could buy a company with the same business model, the same global reach, and similar profit margins—but at a 30% discount?

Meet Komatsu Ltd. (TYO: 6301 / US OTC: KMTUY). Here is why smart value investors are looking at Japan’s No.1 builder instead of chasing the US giant.

First, let’s clear up a misunderstanding. Komatsu is not a small local player. Komatsu is the world’s second-largest manufacturer of construction and mining equipment by market share, trailing only Caterpillar.

Walk past any construction site in Texas, mining operation in Australia, or infrastructure project in Southeast Asia. You will likely see Komatsu’s excavators and dump trucks working right next to Caterpillar’s machines. They are a true global blue-chip company with a reputation for durability and advanced technology (especially in autonomous mining trucks).

This is the most compelling reason to own Komatsu right now. Let’s look at the numbers.

(Note: Please check your brokerage for the latest live data)

The Logic: Investors are paying $15 for every $1 of Caterpillar’s earnings, but only ~$11 for Komatsu’s earnings. Historically, this gap is too wide. By buying Komatsu, you are essentially buying high-quality machinery exposure for “70 cents on the dollar.”

For US investors, the currency situation is a massive bonus. Komatsu generates over 80% of its sales outside of Japan. They sell machines in Dollars and Euros, but their headquarters and many factories are in Japan (paying costs in Yen).

As long as the Yen stays weak, Komatsu enjoys a “cheat code” for profitability that US-based manufacturers simply don’t have.

Komatsu is also a shareholder-friendly company. They have a policy of maintaining a payout ratio of 40% or higher. This means they return a significant portion of their profits directly to you as dividends.

While they may not be a “Dividend Aristocrat” in the strict US sense (due to cyclical earnings), their yield is often competitive with or higher than Caterpillar’s, especially when you buy at today’s depressed valuations.

We are not saying Caterpillar is a bad stock. It is a fantastic company. But as a value investor, price matters.

Why pay a premium for the US leader when you can buy the Global No.2 at a significant discount? If you want exposure to global infrastructure spending and mining without overpaying, Komatsu (6301 / KMTUY) is the logical choice.

The content on this website is for informational and educational purposes only and does not constitute financial, legal, or investment advice. The views expressed are the personal opinions of the author (DividendDan), based on experience as a strategy consultant and individual investor living in Japan.

Market data and company information are subject to change. Please conduct your own due diligence or consult a certified financial advisor before making any investment decisions. The author may hold positions in the securities mentioned.