| Metric | Value |

|---|---|

| Price (JPY) | Y6,469 |

| Dividend Yield | 2.42% |

| P/E Ratio (TTM) | 16.2x |

| Market Cap | Y7.1t |

| 52-Week Range | Y3,240 – Y6,566 |

Educational research only, not investment advice. Market data changes frequently. See the full Disclaimer.

Data freshness: Market prices, yields, valuation multiples, and forecasts in this article are dated snapshots rather than live quotes. Page maintenance review: July 10, 2026. Verify current quotes and the latest official IR guidance before making a decision.

Disclosure: This article contains affiliate links to TradingView. We may earn a commission at no extra cost to you.

ORIX generated ¥447 billion in net income in FY2026 — 27% above the prior year — and simultaneously sold its banking arm for ¥370 billion to redeploy into private equity and renewables. Yet most US investors have never heard of it. Here’s what Japan’s financial disclosures reveal that English-language summaries consistently omit. — DividendDan

Investment Thesis — Data snapshot: May 2026; page maintenance review: July 10, 2026

Author’s View: Constructive | Fair Value Estimate (Author’s Model): ¥5,400–¥5,900 (thesis-based on PBR re-rating toward 1.3× book)

- Core thesis: The ¥370B Orix Bank sale to Daiwa (April 2026) unlocks capital for higher-return segments — PE/concessions, environmental energy, and global asset management — accelerating the shift from spread-income to fee-and-asset-light earnings that TSE reform pressure demands.

- Numeric backing: FY2026 net income +27% YoY to ¥447B; PER 15.9× / PBR 1.56× / yield 2.51% / payout ratio 30.9% — cheap relative to global diversified financial peers.

- Top risk: BOJ rate hikes compress leasing spreads and raise funding costs before bank-sale proceeds are fully redeployed into higher-ROE assets.

| Metric | Value |

|---|---|

| Price (JPY) | Y6,331 |

| Dividend Yield | 2.49% |

| P/E Ratio (TTM) | 15.9x |

| Market Cap | Y6.9t |

| 52-Week Range | Y3,226 – Y6,566 |

ORIX Corporation (TSE: 8591 / NYSE: IX) sits at a genuine inflection point in 2026. Two catalysts — the ¥370 billion divestiture of Orix Bank and the completion of a ¥150 billion share buyback — have landed within months of each other, rewriting the capital structure story for Japan’s most complex diversified financial.

This pillar article maps the full investment landscape: valuation, growth engines, shareholder return mechanics, and the risks that could derail the thesis. It is designed as the analytical hub for the Leasing and Diversified Financials topic cluster on Best Japan Stocks.

Disclosure: This article is for informational purposes only and does not constitute financial advice. See our full Disclaimer before making any investment decisions.

What Is ORIX? A Diversified Financial Conglomerate

Founded in 1964 as a leasing company, ORIX has evolved into one of Japan’s most diversified financial conglomerates. It operates across ten distinct business segments spanning corporate financial services, real estate, environmental energy, insurance, banking, aircraft and ships, and global operations in the U.S., Europe, and Asia.

This breadth is both a strength and a source of complexity. For US dividend investors used to pure-play financials, ORIX requires a different analytical lens — part bank, part private equity firm, part infrastructure operator.

As of March 31, 2026, ORIX reported total revenues of ¥3.33 trillion — a 16% increase year-over-year — and net income attributable to shareholders of ¥447 billion, up 27% YoY. These are not modest numbers for a company trading at 15.9× earnings.

Key primary sources used in this analysis: ORIX Investor Relations | EDINET Filings | FSA (Financial Services Agency) | Minkabu (みんかぶ) (8591) | JPX Market Data

The ¥370 Billion Orix Bank Sale: Why It Changes Everything

In April 2026, ORIX completed the sale of Orix Bank to Daiwa Securities Group for approximately ¥370 billion. To understand why this matters, you need to understand what Orix Bank represented in the portfolio: a spread-income business requiring significant capital to generate relatively low returns.

Spread-income businesses — where you borrow short and lend long — are capital-intensive and rate-sensitive. They compress PBR multiples because the market assigns lower valuations to businesses where earnings are hostage to the yield curve.

By divesting Orix Bank, management is signaling a deliberate pivot toward fee-generating, asset-light segments. The ¥370 billion in proceeds is being redirected into private equity, concessions, environmental energy, and global asset management — all segments with higher potential returns on equity.

This aligns directly with the TSE corporate governance reform framework, which has been pressuring Japanese companies to improve capital efficiency and PBR multiples. ORIX isn’t just complying — it’s using the reform pressure as cover to execute a strategic transformation it arguably wanted to make anyway.

Share Buybacks and Dividend Policy: What the Numbers Say

ORIX has been one of the more aggressive Japanese companies on capital return. The ¥150 billion buyback program completed in 2026 reduced share count meaningfully, providing per-share earnings accretion even before organic growth.

A new repurchase program has been authorized: up to 100,000,000 shares (approximately 9.08% of outstanding shares) for ¥25 billion, running until March 31, 2027. A separate program for up to 40,000,000 shares (3.52%) for ¥100 billion ran until March 2026.

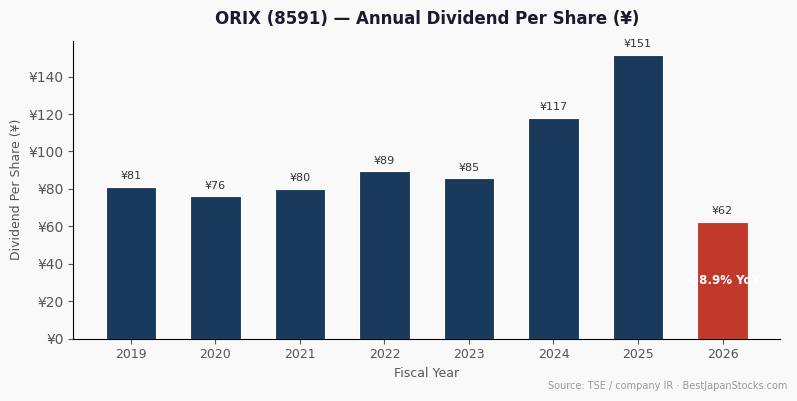

On dividends: the current yield of 2.51% at ¥6,230 reflects a payout ratio of approximately 30.9%. That payout ratio is deliberately conservative — management has room to increase the dividend without straining earnings coverage.

For US dividend investors, the combination of a sub-31% payout ratio and 27% net income growth in FY2026 suggests the dividend is not only sustainable but has meaningful room to grow. You can track the full dividend history at Digrin’s ORIX dividend page.

Segment Deep Dive: Where ORIX Actually Makes Its Money

ORIX operates across ten segments. For investors trying to model the business, the key revenue drivers are Corporate Financial Services and Maintenance Leasing, Real Estate, and the international operations (ORIX USA, ORIX Europe, Asia and Australia).

Corporate Financial Services and Maintenance Leasing remains the core domestic franchise — fleet management, equipment leasing, and SME lending. This segment benefits from Japan’s ongoing corporate capital investment cycle, which is supported by accommodative lending conditions even as the BOJ normalizes rates.

Real Estate is a significant earnings contributor. Office, logistics, and retail real estate in Japan continues to see tight vacancies and rental growth. ORIX’s real estate operations span development, management, and investment — providing multiple revenue streams within the segment.

Environmental Energy is the highest-growth segment. Japan’s energy transition is creating substantial demand for solar, wind, and other renewable infrastructure. ORIX has been building this segment for years and it is now a material contributor to fee income.

Business Investment and Concession includes airport concessions (ORIX operates Kansai International Airport through a consortium) and private equity investments. These are long-duration, fee-generating assets that carry higher valuation multiples than spread-income banking.

ORIX USA and ORIX Europe provide geographic diversification. ORIX USA includes Robeco (asset management) and various private credit and infrastructure businesses. These segments reduce Japan-specific macro dependence.

Japan-Specific Intelligence: What Local Data Tells US Investors

One advantage of this blog is access to Japanese-language data sources that most US investors cannot easily parse. Here is what those sources say about ORIX right now.

Minkabu (みんかぶ) analyst consensus as of May 2026: 5 strongly constructive view, 1 Buy, 3 Neutral — a broadly constructive professional view. The average analyst fair-value estimate is ¥5,923 per Minkabu (みんかぶ), implying approximately -4.9% downside from the May 23 price of ¥6,230.

This is an important signal: professional analysts are constructive but the stock has run ahead of consensus targets. That divergence suggests the recent ~10% surge (reported May 11, 2026) may have pulled forward some of the re-rating thesis.

For a US investor considering entry, the Minkabu consensus implies the near-term upside is limited at current prices — the longer-term thesis (capital reallocation into higher-ROE assets) requires patience.

Minkabu’s AI stock diagnosis rates ORIX as “割高” (overvalued) based on historical and relative comparisons, with a suggested fair-value entry below ¥5,433.

Retail investor sentiment on the platform skews “Sell.” This retail pessimism is notable — it suggests Japanese individual investors are taking profits after the strong run, which could create near-term volatility but does not undermine the structural thesis.

BOJ policy context: The Bank of Japan shifted to raising its policy rate in 2024 and is expected to continue gradual hikes through 2026. The BOJ’s monetary policy meeting minutes confirm the normalization trajectory. For ORIX, rising rates are a double-edged sword:

they compress leasing spreads in the short term but improve returns on the fee-generating and asset management segments over the medium term.

Macroeconomic Tailwinds and Headwinds for 2026

The macro backdrop for ORIX in 2026 is mixed but net positive for a company executing a strategic pivot away from rate-sensitive income.

Tailwinds: Japan’s economy is expected to see moderate growth through 2026, supported by firm private consumption and corporate capital investment.

The car leasing market is projected to grow at a CAGR of approximately 4.97% during 2026–2034, driven by demand for flexible mobility solutions. Japan’s fintech push — including the FSA’s “Japan Fintech Week 2026” initiative — creates opportunities for diversified financial players with digital capabilities.

Headwinds: Accelerated interest rate increases could expand real estate yields, potentially compressing investment returns on ORIX’s property portfolio. Labor shortages and elevated construction costs continue to delay new real estate development.

Globally, financial institutions face rising exposure to non-bank financial institution stress and private credit volatility — relevant given ORIX’s growing PE and private credit footprint.

For US investors, there is an additional layer: yen/dollar exchange rate. A stronger yen boosts the USD value of dividends and capital gains; a weaker yen erodes them. With the BOJ normalizing rates, the yen has structural support — but currency risk remains a real consideration for IRA investors who cannot hedge easily.

Competitive Landscape: How ORIX Stacks Up

ORIX’s closest domestic peers in the leasing and diversified financials space are Tokyo Century Corp (TSE: 8439) and Mitsubishi HC Capital (TSE: 8593). Both compete directly in equipment and vehicle leasing.

Tokyo Century is more narrowly focused on leasing and has a tighter business model, which makes it easier to analyze but limits upside from diversification. Mitsubishi HC Capital has a larger asset base and strong infrastructure financing capabilities — it is arguably the most direct competitor to ORIX’s core leasing franchise.

MUFG (TSE: 8411) competes across ORIX’s lending and corporate finance activities but is primarily a banking group — it does not replicate ORIX’s PE, concession, or environmental energy segments.

ORIX’s differentiation lies in its breadth and its willingness to operate in complex, illiquid asset classes that pure-play lenders avoid. This creates a moat of operational expertise that is difficult to replicate quickly.

Valuation: Is ORIX Cheap, Fair, or Expensive at ¥6,230?

At ¥6,230, ORIX trades at 15.9× trailing earnings and 1.56× book value. The yield is 2.51% with a 30.9% payout ratio.

Compared to global diversified financial peers — think Brookfield Asset Management, Macquarie, or Blackstone — these multiples look modest. Those companies trade at 20–30× earnings with lower yields. The discount reflects Japan-specific risk premiums: governance complexity, yen exposure, and the ongoing business model transition.

The author’s fair-value estimate of ¥5,400–¥5,900 is based on a PBR re-rating toward 1.3× book as the capital reallocation thesis plays out. At current prices of ¥6,230, the stock has already moved above that range — meaning the easy money may have been made. The thesis now requires the higher-ROE segments to deliver on their promise over the next 12–24 months.

Investors can track ORIX’s financial statements and chart history on TradingView, which provides useful context on how the stock has traded relative to book value over time.

TSE Corporate Governance Reform: ORIX as a Compliance Leader

The TSE’s corporate governance reform push has been one of the most significant structural tailwinds for Japanese equities since 2023. The exchange has been pressuring companies trading below 1× book value to improve capital efficiency — and even companies above 1× book to articulate credible plans for sustained improvement.

ORIX has been ahead of this curve. The Orix Bank divestiture, the ¥150 billion buyback completion, and the new 9.08% repurchase authorization all signal a management team that understands what the market wants and is executing accordingly.

For US investors, this is meaningful: TSE reform pressure is a structural tailwind that reduces the risk of capital being trapped in low-return businesses indefinitely. ORIX’s proactive response reduces the governance discount that has historically weighed on Japanese financial conglomerates.

FX Risk and IRA Considerations for US Investors

ORIX trades in Japanese yen on the TSE. For US investors holding ORIX in a taxable account or IRA, every dividend payment and any eventual capital gain or loss will be converted from yen to dollars at the prevailing exchange rate.

The yen has been weak against the dollar for much of 2023–2025, which has reduced the USD-denominated returns for US holders. However, BOJ rate normalization is expected to provide structural yen support going forward. A move from ¥155/USD toward ¥130–¥140/USD would add meaningful USD-equivalent returns on top of the yen-denominated thesis.

Japan withholds tax on dividends paid to U.S. (non-resident) investors at a statutory rate of 15.315% (15% base rate + 0.315% reconstruction surtax).

U.S. individual investors holding portfolio positions may qualify for a reduced 10% treaty rate under the U.S.–Japan tax treaty (Article 10), but the lower rate applies only if your broker has collected the required treaty documentation (Form W-8BEN or equivalent); in practice, many retail investors receive the full 15.315% withheld at source.

The withheld amount is generally eligible for the foreign tax credit (IRS Form 1116) in taxable brokerage accounts; it is not recoverable in tax-advantaged accounts such as IRAs or 401(k)s.

Japan Edge: ORIX Local-Source Checklist for 2026

The English-language ORIX story often compresses the company into a broad “leasing and financials” label. The Japan Edge is more specific:

ORIX is a diversified capital allocator listed on the TSE Prime Market, and Japanese sources let investors check whether the thesis is being driven by recurring business earnings, portfolio reshuffling, capital returns, or local sentiment.

That distinction matters because ORIX can look inexpensive or income-oriented while a meaningful part of profit still comes from investment gains, exits, insurance, real estate, aircraft, concessions, and overseas units.

The latest ORIX annual results give the concrete starting point. For the fiscal year ended March 31, 2026, ORIX reported net income attributable to ORIX shareholders of ¥447.265 billion, up 27.2% year over year, with ROE of 10.4% and basic EPS of ¥400.27.

The company also guided to ¥530 billion of net income for the fiscal year ending March 31, 2027 and presented an estimated annual dividend of ¥187.36 per share, based on a 39% payout framework and the FY2027 profit forecast. Those figures turn ORIX from a generic value stock into a measurable capital-return and earnings-quality test.

| Local source | What to verify | Investor takeaway |

|---|---|---|

| ORIX FY2026 results | FY2026 net income ¥447.265bn, ROE 10.4%, EPS ¥400.27, FY2027 net income forecast ¥530bn | The bull case needs profit growth beyond one-time investment gains; compare each quarter against the ¥530bn full-year target. |

| Dividend framework | FY2026 dividend ¥156.10; FY2027 estimate ¥187.36 under the 39% payout approach | Income support is meaningful, but dividend growth depends on earnings delivery and share-count changes. |

| EDINET annual securities report | Segment risk, overseas exposure, investment securities, governance, and statutory Japanese disclosure | Use EDINET to confirm whether earnings quality and risk language match the cleaner IR presentation. |

| JPX/TSE listing context | 8591 is a TSE Prime name with Japan governance and disclosure expectations | ORIX should be judged on capital efficiency, shareholder returns, and disclosure progress, not just headline yield. |

| みんかぶ 8591 | Local snapshot showed a 6,481 yen price, 5,730 yen reference value, 2.89% dividend yield, PER 16.19x, PBR 1.62x, and market cap ¥7.285tn on July 10, 2026 | Domestic sentiment was not simply “cheap Japan financial”; the local page framed valuation as stretched even while analysts remained constructive. |

Watch and Verify Actions

- Quarterly earnings bridge: after each ORIX quarterly release, compare cumulative net income with the ¥530 billion FY2027 target and identify whether gains came from recurring segment profit or investment exits.

- Capital-return math: update the dividend case when ORIX reports share repurchases or treasury-share changes, because the FY2027 dividend estimate depends partly on the number of shares excluding treasury stock.

- Segment mix: separate stable domestic finance, maintenance leasing, insurance, real estate, aircraft/ships, ORIX USA, Europe, and Asia/Australia. A higher consolidated profit number is less valuable if it is concentrated in hard-to-repeat investment gains.

- EDINET cross-check: read the Japanese annual securities report for risk factors, investment securities, and governance detail before treating the English IR deck as the whole story.

- Local sentiment check: use みんかぶ and JPX/TSE pages as a reality check on valuation and domestic framing, especially when the stock trades above local reference-value snapshots.

Investor takeaway: ORIX can still work for U.S. investors as a diversified Japan financial with shareholder-return discipline, but the edge comes from verifying the source of profit.

A clean upgrade would be sustained progress toward the FY2027 ¥530 billion net-income target, ROE holding above 10%, and dividend growth supported by recurring earnings.

A warning sign would be a higher share price driven mainly by local yield demand while EDINET and segment disclosures show profit leaning too heavily on disposals or market-sensitive investment gains.

Risks and Counter-View

A constructive view on ORIX requires acknowledging three substantive risks that could impair the thesis:

1. BOJ rate hike pace exceeds expectations. If the BOJ raises rates faster than the market anticipates, leasing spreads compress more sharply and ORIX’s funding costs rise before the bank-sale proceeds are fully redeployed. This is the single most important near-term risk to monitor.

2. Capital reallocation execution risk. The ¥370 billion from the Orix Bank sale needs to be deployed into higher-ROE assets. If management overpays for PE assets or renewable energy projects, or if those segments underperform, the re-rating thesis fails. History shows that large capital reallocation programs often take longer and deliver less than planned.

3. Stock has run ahead of consensus. As noted above, Minkabu’s analyst consensus target of ¥5,923 implies the stock is already trading above fair value at ¥6,230. The Minkabu AI diagnosis of “割高” (overvalued) and retail “Sell” sentiment suggest limited near-term upside and potential for a pullback. This does not invalidate the long-term thesis but does affect entry-point timing.

4. Global private credit stress. ORIX’s growing exposure to non-bank financial institution assets and private credit creates tail risk if global credit conditions deteriorate. This is a lower-probability but higher-impact scenario worth monitoring.

Bottom Line — Author’s View: Constructive with Patience Required

ORIX at ¥6,230 is a structurally improving business trading at 15.9× earnings and 1.56× book, with a 27% net income growth print in FY2026 and a 30.9% payout ratio that leaves ample room for dividend increases.

The Orix Bank divestiture is the most important strategic event in ORIX’s recent history. It signals a management team willing to sacrifice near-term spread income to build a more valuable, fee-generating franchise — exactly what TSE reform pressure and global investors are demanding.

However, the stock’s recent ~10% surge has pulled it above the author’s fair-value estimate range of ¥5,400–¥5,900 and above the Minkabu analyst consensus target of ¥5,923. At current prices, the risk/reward is less compelling than it was three months ago. A patient investor might consider waiting for a pullback toward ¥5,500–¥5,700 before building a full position.

For US dividend investors with a 3–5 year horizon, ORIX offers a rare combination: Japan-specific diversification, a credible capital reallocation story, a conservative payout ratio with room to grow, and a management team that is actively responding to governance reform pressure.

The 2.51% yield is modest today — but if earnings continue growing at double-digit rates and the payout ratio expands modestly, the yield-on-cost picture improves significantly over time.

Frequently Asked Questions

What are the US tax implications of receiving ORIX dividends?

Under the US-Japan tax treaty, Japanese dividend withholding is reduced to 15.315% for eligible US investors. You can claim this as a foreign tax credit on IRS Form 1116, effectively offsetting the withholding against your US tax liability. If holding the ADR (NYSE: IX), confirm with your broker that the treaty rate is being applied — some custodians default to the full 15.315% Japanese rate.

Consult a tax professional for your specific situation.

Is ORIX accessible in a US IRA account?

Yes. US investors can access ORIX via the NYSE ADR (ticker: IX) through most US brokerages, including those that support IRA accounts. Direct TSE access (ticker: 8591) is available through Interactive Brokers and Saxo Bank. Note that foreign tax credits are not claimable in a tax-deferred IRA — the 15.315% withholding becomes an unrecoverable cost in that account structure.

What does the Minkabu analyst consensus say about ORIX?

As of May 2026, Minkabu shows 5 strongly constructive view, 1 Buy, and 3 Neutral ratings among professional analysts, with an average fair-value estimate of ¥5,923 — implying approximately -4.9% downside from the current price of ¥6,230. This suggests the stock has run ahead of professional consensus following its recent surge.

The Minkabu AI diagnosis rates ORIX as “割高” (overvalued) at current prices, with a suggested entry below ¥5,433.

How to Buy 8591 from the U.S.

ORIX Corp (8591) trades on the Tokyo Stock Exchange and is also available to U.S. investors as an ADR under the ticker IX through major U.S. brokers. For direct TSE access, international. For step-by-step brokerage setup, ADR vs. direct TSE shares, and U.S. tax handling, see our complete guide: How to Buy Japanese Stocks from the U.S..

Related Articles

- MUFG (8306): The 2026 Hub Analysis for Japan’s Megabanks

- How U.S. Investors Can Buy Sumitomo Mitsui (8316) at 4%+ Yield in 2026

- Mitsubishi Corp (8058): The 2026 Hub Analysis for Trading Houses

- 5 Japanese Dividend Aristocrats for 2026: A Practical Framework for Foreign Investors

- How U.S. Investors Can Buy KDDI (9433) at 3%+ Yield in 2026

Data snapshot: May 2026; page maintenance review: July 10, 2026. This article is for informational purposes only and does not constitute investment advice. Opinions are my own. I do not currently hold positions in securities mentioned. All investments involve risk, including loss of principal. Past performance is not indicative of future results.

This disclosure is made in accordance with FTC 16 CFR Part 255. See our full Disclaimer for complete disclosures.