| Metric | Value |

|---|---|

| Price (JPY) | Y7,609 |

| Dividend Yield | 3.11% |

| P/E Ratio (TTM) | 27.2x |

| Market Cap | Y14.5t |

| 52-Week Range | Y5,300 – Y8,038 |

Educational research only, not investment advice. Market data changes frequently. See the full Disclaimer.

Data freshness: Market prices, yields, valuation multiples, and forecasts in this article are dated snapshots rather than live quotes. Page maintenance review: July 10, 2026. Verify current quotes and the latest official IR guidance before making a decision.

| Metric | Value |

|---|---|

| Price (JPY) | Y7,584 |

| Dividend Yield | 3.26% |

| P/E Ratio (TTM) | 27.1x |

| Market Cap | Y14.5t |

| 52-Week Range | Y5,300 – Y8,038 |

¥980.4 billion in full-year net income. A ¥287 billion Berkshire Hathaway strategic stake finalized in May 2026. A 3.07% trailing dividend yield on a stock that barely registers in US financial media. Tokio Marine (8766) is hiding in plain sight — and the gap between what Japanese IR documents reveal and what English coverage captures is still very, very wide. — DividendDan

Investment Thesis

Author’s View: Constructive | Fair Value Estimate (Author’s Model): ¥8,000–¥8,500 (Minkabu (みんかぶ) analyst consensus: ¥8,232)

- Berkshire Hathaway’s NICO finalized a ¥287 billion strategic treasury share allotment in May 2026 — covering reinsurance collaboration and a joint M&A pipeline, not passive equity holding. International insurance now drives ~69% of business unit profit growth.

- Full-year FY2026: ¥980.4B net income on approximately ¥8.9T revenue (FY2026, ended March 2026); trailing P/E 13.79x; dividend yield 3.07%; payout ratio 42%; 10-year DPS CAGR 19.4% per company IR.

- Top risk: US hurricane and wildfire concentration via Pure Group could spike catastrophe losses sharply in any single severe-weather year.

Data snapshot: May 2026; page maintenance review: July 10, 2026

| Metric | Value |

|---|---|

| Stock Price (JPY) | ¥7,116 (May 29, 2026) |

| Dividend Yield (Trailing) | 3.07% |

| P/E Ratio (TTM) | 13.79x |

| Market Cap | ¥13.75 trillion |

| 52-Week Range | ¥5,300 – ¥7,870 |

| Payout Ratio | 42.28% |

| 10-Year DPS CAGR | 19.4% (per company IR) |

Tokio Marine Holdings (TSE: 8766 / OTC: TKOMY) is simultaneously Japan’s largest non-life insurer, a rapidly internationalizing specialty insurance platform, and — as of May 2026 — a confirmed Berkshire Hathaway strategic partner.

Read our full Disclaimer before proceeding. This is investment analysis, not financial advice. The author’s position disclosure appears at the end of this article.

The Berkshire NICO Stake: Strategic Partnership, Not a Passive Bet

In May 2026, Tokio Marine finalized a ¥287 billion treasury share allotment to Berkshire Hathaway’s National Indemnity Company (NICO). This was not a simple open-market purchase.

The arrangement covers reinsurance collaboration and a joint M&A pipeline — making NICO an operational partner, not merely a financial investor. The structure resembles how Berkshire deploys insurance float to fund acquisitions globally.

On the same day (May 25, 2026), Tokio Marine unveiled “Aspiration 2035,” a decade-long strategic vision targeting sustainable profit growth and social impact. The company was simultaneously designated an “SX Brand 2026” by METI and the TSE — a recognition reserved for companies demonstrating sustainable value creation, awarded to fewer than 50 Japanese companies.

Separately, the board approved a ¥200 billion share repurchase program covering up to 130 million shares (~6.9% of outstanding) through December 2026. Combined, this is an unusually dense capital-allocation signal in a single week.

This remains pure pattern-matching analysis based entirely on public disclosures. I have no insider knowledge of Berkshire’s forward intentions. Investors should not buy 8766 on the assumption that Berkshire will increase its stake further.

Business Model: Float-Funded Global Insurance

Tokio Marine operates across four segments: Domestic Non-Life, Domestic Life, International Insurance, and Financial & Other. As detailed in Japanese-language IR materials (東京海上ホールディングス IR), the International segment drove approximately 69% of business unit profit growth in FY2025 projections.

North American specialty insurance — anchored by the Pure Group acquisition — now leads international profit generation. Pure focuses on high-net-worth homeowners: premium pricing power, but meaningful hurricane and wildfire concentration risk discussed in the Risks section below.

The domestic Japan business remains a stable cash generator. S&P Global’s stable 2026 outlook for Japanese non-life insurers cites stronger balance sheets, growing demand for cyber coverage, and infrastructure-driven catastrophe policies as structural tailwinds.

TSE corporate governance reforms are also accelerating capital efficiency. Tokio Marine is unwinding cross-shareholdings (business-related equities) to zero by FY2029 — a direct response to TSE pressure — and reallocating freed capital to core operations and shareholder returns.

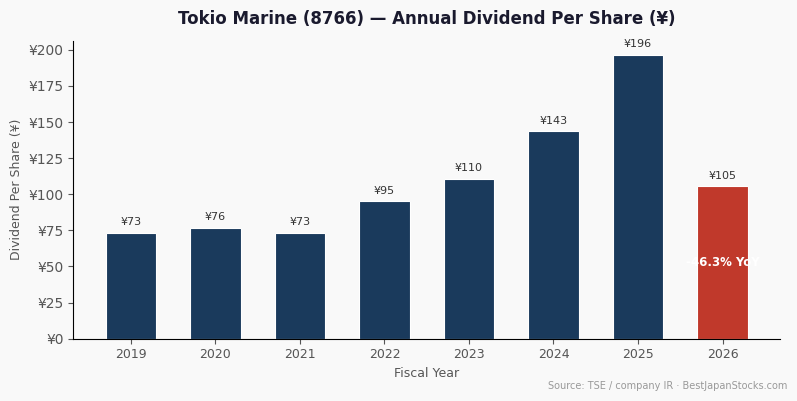

Dividend Track Record and Capital Return Policy

Tokio Marine’s 10-year DPS CAGR of 19.4% ranks among the highest in the Japanese non-life insurance sector, per company IR data. The trailing dividend yield stands at 3.07% at the May 29, 2026 price of ¥7,116.

Full-year FY2026 (ended March 31, 2026) delivered ¥980.4 billion in net income on approximately ¥8.9 trillion in revenue (FY2026, ended March 2026). Net income declined 7.1% YoY, reflecting catastrophe normalization and FX headwinds. Full-year EPS was ¥516 versus ¥542 in FY2025.

The payout ratio of 42.28% sits meaningfully below the company’s stated 50% target. That buffer allows Tokio Marine to grow dividends faster than earnings in softer years — the structural engine behind the 19.4% 10-year DPS CAGR.

Capital returns over the past 12 months included approximately ¥417 billion in buybacks. Layering the new ¥200 billion program on top signals management’s continued conviction in intrinsic value well above current market pricing.

Japan Edge: What English Sources Miss

Minkabu (みんかぶ) analyst consensus: Professional analysts tracked on Minkabu (みんかぶ) set a consensus fair-value estimate of ¥8,232 with a “Buy” rating — implying approximately +15.7% upside from the May 29 price of ¥7,116.

That implied upside, layered on a 3.07% trailing yield, confirms that professional Japanese analysts view current earnings and dividend capacity as not fully priced in. For a US-based income investor who can’t easily access Minkabu directly, this margin-of-safety signal is exactly the kind of edge this blog exists to surface.

Yahoo!ファイナンス 掲示板 sentiment: Post-earnings retail discussion on Yahoo!ファイナンス 掲示板 (Japanese bulletin board) turned cautious after the stock fell from ¥7,817 (May 20 peak) to ¥7,116 (May 29).

Comments attribute the slide to “sell-the-news” behavior following the capital return announcements. This institutional-announcement-then-retail-pullback pattern recurs regularly in large Japanese financial stocks and has historically created re-entry windows rather than signaling fundamental deterioration.

Investors tracking 8766’s price action on TradingView will note the RSI cooling from overbought territory following the May 20 peak — technical positioning that may attract contrarian buyers in the near term.

EDINET filings: Tokio Marine’s full 有価証券報告書 (annual securities reports) are publicly available in Japanese on EDINET (FSA Japan). These contain granular segment-level revenue and loss data not always reproduced in English IR summaries — useful for verifying management’s catastrophe loss assumptions.

OpenWork employee satisfaction: A publicly accessible overall score for 東京海上ホールディングス on OpenWork.jp was not surfaced in current search results — an open data gap we will update in future revisions.

Risks and Counter-View

1. US catastrophe concentration. Pure Group’s high-net-worth homeowner book is exposed to US hurricane and wildfire seasons. A severe-weather year comparable to 2022 could spike claims and compress full-year net income materially — the FY2026 7.1% earnings decline is a reminder that this risk is not theoretical.

2. FX erosion for USD investors. Dividends are paid in yen. A sustained strong-dollar environment erodes real USD returns on TKOMY ADR positions. The 3.07% trailing yield could compress to 2.5% or below in a USD bull cycle without any change in yen-denominated dividend policy.

3. Earnings declined 7.1% in FY2026 despite revenue growth. Revenue rose +4.6% but net income fell. Bears correctly note that insurance profitability is lumpy: catastrophe normalization can persist across multiple fiscal years and compress the payout ratio buffer faster than management’s 50% target implies.

4. Data governance incident. In April 2026, staff from a Tokio Marine unit seconded to Toyota were found to have removed proprietary data without authorization, triggering an internal probe. The financial impact is likely immaterial, but governance incidents attract elevated scrutiny from ESG-focused institutional investors in the TSE reform era — and reputational risk is real in the Japanese market.

Bottom Line — Author’s View on 8766 for 2026

Constructive. At ¥7,116 and a trailing P/E of 13.79x, Tokio Marine offers a 3.07% dividend yield anchored by a 42% payout ratio that sits well below management’s own 50% ceiling. The 10-year DPS CAGR of 19.4% gives income investors a credible growth trajectory that few global insurance peers can match.

The Berkshire NICO strategic partnership adds a quality validation signal. It is not a guaranteed re-rating catalyst — but it is structurally consistent with the thesis that global institutional capital is underweighting Tokio Marine relative to intrinsic value.

Layering the Minkabu (みんかぶ) consensus upside of ~16% onto the 3.07% trailing yield points to a plausible 19%+ total return scenario if earnings stabilize and yen weakness moderates. For a US dividend investor aged 50–65 seeking international income diversification alongside domestic holdings, this risk-reward profile warrants a serious look as a sub-5% portfolio allocation — with both eyes open on hurricane season and yen moves.

Frequently Asked Questions

Q: How does Japanese dividend withholding tax affect US investors?

A: Japan withholds 15.315% on dividends paid to foreign investors. US investors can claim this as a foreign tax credit on IRS Form 1116 to offset federal tax liability. Treatment may vary between the TKOMY ADR and direct TSE holdings — consult a tax professional familiar with foreign equity income.

Q: Is there a US-accessible ADR for Tokio Marine?

A: Yes. Tokio Marine trades OTC in the US as TKOMY (ADR). For tighter spreads and more transparent pricing, direct TSE access through IBKR or Saxo Bank is preferred — it requires a JPY conversion step but avoids ADR program fees and potential spread widening on thin OTC volume.

Q: What is the biggest single risk for a US-based Tokio Marine investor?

A: The combination of US catastrophe exposure (hurricanes and wildfires via Pure Group) and JPY/USD currency risk. A severe hurricane season coinciding with a strong-dollar year could meaningfully compress USD-denominated total returns in a single fiscal year — without any deterioration in the underlying yen-denominated business.

Q: Does Tokio Marine offer 株主優待 (kabunushi yutai) shareholder perks?

A: No. Tokio Marine does not offer shareholder perks — typical for large Japanese financial companies. The entire investor case rests on dividends and capital appreciation. US shareholders face no disadvantage on this dimension compared to Japanese retail investors.

How to Buy 8766 from the U.S.

Tokio Marine Holdings (8766) trades on the Tokyo Stock Exchange Prime Market and is also available to U.S. investors as an OTC ADR under the ticker TKOMY. For direct exposure to the TSE-listed. For step-by-step brokerage setup, ADR vs. direct TSE shares, and U.S. tax handling, see our complete guide: How to Buy Japanese Stocks from the U.S..

Japan withholds tax on dividends paid to U.S. (non-resident) investors at a statutory rate of 15.315% (15% base rate + 0.315% reconstruction surtax).

U.S. individual investors holding portfolio positions may qualify for a reduced 10% treaty rate under the U.S.–Japan tax treaty (Article 10), but the lower rate applies only if your broker has collected the required treaty documentation (Form W-8BEN or equivalent); in practice, many retail investors receive the full 15.315% withheld at source.

The withheld amount is generally eligible for the foreign tax credit (IRS Form 1116) in taxable brokerage accounts; it is not recoverable in tax-advantaged accounts such as IRAs or 401(k)s.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial advice or a solicitation to buy or sell any security. Opinions are my own and not investment advice. Current position information is not provided for this article; do not infer a holding from the thesis. No compensation was received from Tokio Marine Holdings, its affiliates, Berkshire Hathaway, or any broker mentioned in this article. Investing in foreign equities involves currency risk, political risk, liquidity risk, and market risk. Past dividend growth does not guarantee future dividend payments. Consult a licensed financial advisor before making any investment decisions. See our full Disclaimer for complete disclosures. Compliant with FTC 16 CFR Part 255. Data snapshot: May 2026; page maintenance review: July 10, 2026.