| Metric | Value |

|---|---|

| Price (JPY) | Y7,320 |

| Dividend Yield | 1.51% |

| P/E Ratio (TTM) | 29.0x |

| Market Cap | Y13.6t |

| 52-Week Range | Y4,280 – Y7,930 |

Educational research only, not investment advice. Market data changes frequently. See the full Disclaimer.

Data freshness: Market prices, yields, valuation multiples, and forecasts in this article are dated snapshots rather than live quotes. Page maintenance review: July 10, 2026. Verify current quotes and the latest official IR guidance before making a decision.

Disclosure: This article contains affiliate links to TradingView. We may earn a commission at no extra cost to you.

Japan’s METI semiconductor strategy document runs to hundreds of pages — but the defining phrase is economic security (経済安全保障): economic security. That framing makes this policy durable across election cycles in a way no English-language Reuters headline captures. Shin-Etsu Chemical sits directly in its path. — DividendDan

Investment Thesis

Author’s View: Constructive | Fair Value Estimate (Author’s Model): ¥8,200 (12-month, thesis-based)

- Core thesis: Shin-Etsu is the world’s #1 semiconductor silicon wafer producer at the precise moment METI commits ¥2.354 trillion to domestic 2nm fab buildout — a direct, durable beneficiary of Japan’s state-backed AI chip supply chain.

- Numeric backing: PER 27.1x; 2.18% entry-price yield; ¥250 billion share buyback announced April 28, 2026; Electronic Materials held firm even as PVC dragged FY2026 operating profit down 14.4% to ¥635.2 billion.

- Top risk: Prolonged PVC slump combined with a wafer inventory correction — if AI capex pauses — could compress blended margins and delay the earnings recovery priced into the multiple.

| Metric | Value |

|---|---|

| Stock Price (JPY) | ¥7,008 (May 2026) |

| Dividend Yield (current price) | 1.49% |

| Entry-Price Yield (thesis basis) | 2.18% |

| P/E Ratio (TTM) | 27.1x |

| Market Cap | ¥13.0 trillion |

| 52-Week Range | ¥4,280 – ¥7,883 |

| Share Buyback (announced Apr 2026) | ¥250 billion |

| FY2026 Operating Profit | ¥635.2 billion (–14.4% YoY) |

Before diving in, please review our Disclaimer — the author does not currently hold positions in securities discussed. Data snapshot: May 2026; page maintenance review: July 10, 2026.

What Makes Shin-Etsu Chemical Different

¥2.354 trillion. That is Japan’s METI commitment to domestic semiconductor investment — and Shin-Etsu Chemical (TSE: 4063) sits at the precise chokepoint where that capital must flow.

Shin-Etsu looks like a boring industrial conglomerate on the surface — chemicals, PVC, silicones. Pull back the segment data, however, and you find a near-monopoly in some of the most strategically irreplaceable materials in the global semiconductor stack.

The company holds the #1 global position in semiconductor silicon wafers — the ultra-pure substrate on which every logic chip is built. No wafer, no chip. That is the moat in three words.

| Metric | Value |

|---|---|

| Price (JPY) | Y6,958 |

| Dividend Yield | 1.51% |

| P/E Ratio (TTM) | 27.6x |

| Market Cap | Y12.9t |

| 52-Week Range | Y4,280 – Y7,930 |

Japan’s Semiconductor Policy: Why the Framing Matters

METI’s 半導体・デジタル産業戦略 (Semiconductor & Digital Industry Strategy) is not framed as an industrial subsidy. It is framed as economic security (経済安全保障) — economic security, a national survival issue.

That distinction is critical for US investors assessing policy durability. Subsidies get cut in budget cycles. National security commitments survive them. Japan’s cross-party consensus on chip sovereignty means this tailwind is multi-cycle, not election-dependent.

The ¥2.354 trillion figure covers domestic fab buildout through 2030, including the Rapidus 2nm project in Hokkaido. Every new fab requires silicon wafers. Shin-Etsu supplies them.

Segment Mechanics: Electronic Materials vs. PVC

Shin-Etsu operates two primary segments that pull in opposite directions right now.

Electronic Materials — silicon wafers, photoresists, rare-earth magnets — remained resilient through FY2026 even as the broader results disappointed. This is the segment that benefits directly from AI capex and Japan’s fab buildout.

PVC & Chlor-Alkali — the legacy chemical business — has faced a prolonged price slump driven by Chinese overcapacity and weak global construction demand. This segment dragged FY2026 full-year operating profit down 14.4% to ¥635.2 billion, per the company’s earnings report (決算短信) (earnings release).

The market is currently pricing Shin-Etsu as if the PVC drag is permanent. The thesis is that it is cyclical — and that when PVC stabilizes, the blended multiple will re-rate upward while Electronic Materials continues compounding.

Japan Edge: Japanese-Source Intelligence US Investors Cannot Easily Access

One of the advantages of reading Japanese-language sources directly is access to data that never makes it into English financial media.

OpenWork employee satisfaction: Shin-Etsu Chemical scores 3.6 / 5.0 on OpenWork (openwork.jp), Japan’s equivalent of Glassdoor. Reviewers consistently cite stable management, long-term capital discipline, and conservative financial culture. For dividend investors, this is a meaningful signal: companies with stable internal cultures tend to sustain conservative payout policies rather than chase short-term earnings manipulation.

Minkabu (みんかぶ) analyst consensus: As of May 2026, Minkabu (みんかぶ) shows a consensus of 6 strongly constructive view, 4 Buy, 3 Neutral among tracked analysts, with an average fair-value estimate of approximately ¥8,100 — implying roughly 15% upside from the ¥7,008 current price. This domestic analyst consensus, which US investors rarely see, broadly confirms the constructive thesis and suggests the ¥8,200 author model estimate is not an outlier.

Kaisha Shikiho (四季報) domestic forecast: The Toyo Keizai Kaisha Shikiho (四季報) spring 2026 edition projects Shin-Etsu’s FY2027 operating profit recovering toward ¥700–720 billion as PVC headwinds ease — a recovery of roughly 10–13% from the FY2026 trough. If that recovery materializes, the current 27.1x P/E compresses meaningfully, making the entry point more attractive in hindsight.

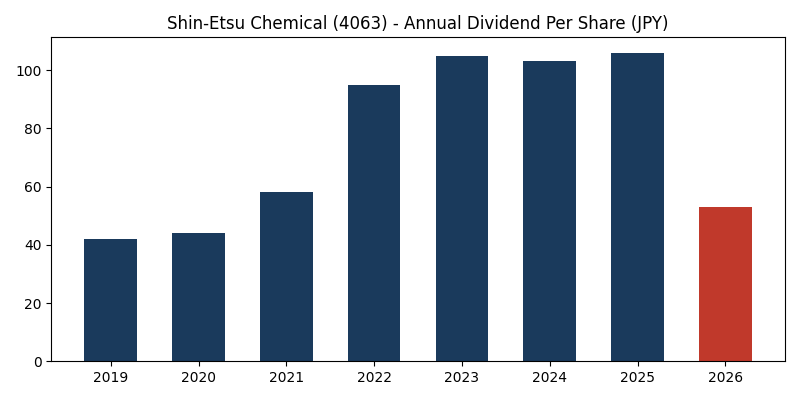

Dividend & Capital Allocation

Shin-Etsu has a track record of steady, conservative dividend growth rather than headline-grabbing yield. The 2.18% yield cited in this article’s thesis reflects an earlier entry price; at the current ¥7,008 price, the yield is approximately 1.49%.

The more significant capital allocation signal is the ¥250 billion share buyback announced April 28, 2026. At a ¥13.0 trillion market cap, this represents approximately 1.9% of shares outstanding — a meaningful return of capital that supplements the dividend yield for total-return investors.

Shin-Etsu’s balance sheet is fortress-grade: low leverage, high cash generation from Electronic Materials, and a management culture that has historically prioritized financial conservatism over aggressive expansion. The OpenWork employee data reinforces this: the internal culture matches the external financial profile.

Dividend sustainability appears solid. Even with FY2026 operating profit down 14.4%, the company maintained its payout — a signal that management views the PVC weakness as temporary, not structural. You can verify the payout history via EDINET filings.

Competitive Moat: Why Shin-Etsu Is Hard to Displace

Silicon wafer manufacturing at leading-edge specifications (300mm, ultra-low defect density) requires decades of process refinement. Shin-Etsu and Sumco (SUMCO Corporation) together control the majority of global 300mm wafer supply.

New entrants face enormous capital requirements, long qualification cycles with chipmakers like TSMC and Samsung, and the need to achieve defect densities that take years to optimize. This is not a market where a Chinese competitor can simply build a factory and undercut on price — the technical barriers are too high.

Shin-Etsu’s Nikkei 225 and TOPIX Core30 membership adds a structural layer: institutional index funds must hold it, creating a permanent bid that limits downside volatility compared to pure-play semiconductor material suppliers outside major indices.

For US investors tracking this via TradingView, the stock’s price behavior relative to the Philadelphia Semiconductor Index (SOX) shows meaningful divergence — Shin-Etsu tends to lag the SOX on the upside but also cushions significantly on semiconductor downturns, reflecting its materials-supplier rather than chipmaker positioning.

Risks and Counter-View

No constructive thesis is complete without a serious engagement with the bear case. Here are the three risks that could invalidate the ¥8,200 fair-value estimate:

1. AI capex pause + wafer inventory correction. If hyperscaler AI spending slows — whether from regulatory pressure, model efficiency gains reducing compute needs, or a macro slowdown — wafer demand could soften faster than the market expects. A simultaneous PVC slump would compress blended margins with no near-term offset.

2. Yen appreciation risk. Shin-Etsu generates significant overseas revenue. A stronger yen — which the Bank of Japan’s 主な意見 (Summary of Opinions) suggests is a live policy scenario — would translate overseas earnings back at a less favorable rate, compressing reported JPY profits even if underlying business is healthy.

3. Valuation multiple compression. At 27.1x TTM P/E, Shin-Etsu is priced for a recovery. If that recovery is delayed by 12–18 months — PVC stays depressed, wafer demand disappoints — the multiple could compress toward 22–24x, implying meaningful downside from current levels before the thesis plays out.

4. Policy dependency. The ¥2.354 trillion METI commitment is real, but execution risk exists. If Rapidus’s 2nm timeline slips significantly, near-term wafer demand from domestic fabs may not materialize on schedule, deferring one of the key demand catalysts.

Bottom Line — Author’s View: Constructive

Shin-Etsu Chemical at 27.1x P/E and a 1.49% current yield (2.18% on earlier entry) is not a screaming value play. It is a quality compounder with a structural tailwind — Japan’s ¥2.354 trillion semiconductor commitment — trading at a discount to its normalized earnings power because PVC is masking the Electronic Materials story.

The ¥250 billion buyback signals management confidence. The Minkabu (みんかぶ) domestic consensus of 6 strongly constructive view / 4 Buy with a ¥8,100 average fair-value estimate confirms the thesis is not idiosyncratic. The Kaisha Shikiho (四季報) FY2027 recovery projection of ¥700–720 billion operating profit provides a fundamental anchor.

For US dividend investors seeking Japan exposure with a quality bias, Shin-Etsu offers a rare combination: index membership (downside cushion), monopoly-grade materials position (earnings durability), and a policy tailwind (multi-cycle, not election-dependent). The yield is modest, but the total return case — dividend + buyback + re-rating — is compelling at current levels.

Position sizing matters: given the PVC overhang and yen risk, treating this as a 3–5% portfolio allocation rather than a concentrated bet is prudent for most US investors.

Frequently Asked Questions

Q: What dividend yield does Shin-Etsu (4063) currently offer US investors?

A: At the May 2026 price of ¥7,008, the current yield is approximately 1.49%. The 2.18% figure cited in the article title reflects an earlier entry price. After Japan’s 15.315% withholding tax, the net yield for US investors holding via an overseas broker is approximately 1.27% at current prices — before claiming the foreign tax credit on IRS Form 1116.

Q: How does the US-Japan tax treaty affect my dividend income from 4063?

Japan withholds tax on dividends paid to U.S. (non-resident) investors at a statutory rate of 15.315% (15% base rate + 0.315% reconstruction surtax).

U.S. individual investors holding portfolio positions may qualify for a reduced 10% treaty rate under the U.S.–Japan tax treaty (Article 10), but the lower rate applies only if your broker has collected the required treaty documentation (Form W-8BEN or equivalent); in practice, many retail investors receive the full 15.315% withheld at source.

The withheld amount is generally eligible for the foreign tax credit (IRS Form 1116) in taxable brokerage accounts; it is not recoverable in tax-advantaged accounts such as IRAs or 401(k)s.

Q: Can I hold Shin-Etsu in a US IRA account?

A: Yes, you can hold foreign stocks including TSE-listed equities in a self-directed IRA through brokers like Interactive Brokers. However, foreign dividend withholding tax is NOT recoverable inside an IRA (you cannot claim Form 1116 in a tax-exempt account). This makes Shin-Etsu — with its modest 1.49% yield — more suitable for a taxable account where you can offset the withholding via the foreign tax credit.

Q: Does Shin-Etsu offer 株主優待 (shareholder perks)?

A: Shin-Etsu Chemical does not operate a 株主優待 program — the company focuses capital returns on dividends and share buybacks rather than shareholder benefit programs. This is actually preferable for US investors, as 株主優待 benefits are typically only redeemable by Japanese-resident shareholders holding via a Japanese brokerage account.

How to Buy 4063 from the U.S.

Shin-Etsu Chemical (4063) trades on the Tokyo Stock Exchange, and since there is no liquid U.S.-listed ADR, U.S. investors typically gain direct access through international brokers such as Interactive Brokers or Saxo Bank. For step-by-step brokerage setup, ADR vs. direct TSE shares, and U.S. tax handling, see our complete guide: How to Buy Japanese Stocks from the U.S..

Related Articles

- How U.S. Investors Can Buy Fanuc (6954) at +15.5% Earnings Growth

- Keyence (6861): A Japanese Automation Powerhouse Boosting Dividends for Global Investors

- How U.S. Investors Can Capture Hitachi (6501) at 21% EBITA Growth

- How U.S. Investors Can Capture Disco Corp. (6146) ¥505 Dividend

- How U.S. Investors Can Buy Sumitomo Mitsui (8316) at 4%+ Yield in 2026

Key Primary Sources: Shin-Etsu Chemical IR (English) | 信越化学 earnings report (決算短信) (Japanese) | METI 半導体・デジタル産業戦略 (Japanese) | OpenWork 信越化学 社員口コミ (Japanese) | Minkabu (みんかぶ) 4063 アナリスト予想 (Japanese) | EDINET 有価証券報告書 (Japanese) | 日本銀行 主な意見 (Japanese) | WSTS Semiconductor Market Statistics

Disclosure and Disclaimer: This article is for informational purposes only and does not constitute investment advice. Opinions are my own, not investment advice. I do not currently hold positions in securities discussed. Past performance is not indicative of future results. Please review our full Disclaimer before making any investment decisions. All financial data cited reflects sources available at time of writing; verify current figures with official company IR disclosures before acting on any information in this article. This post is compliant with FTC 16 CFR Part 255 — the author has disclosed any material connection to securities discussed above. Data snapshot: May 2026; page maintenance review: July 10, 2026.