Data freshness: Market prices, yields, valuation multiples, and forecasts in this article are dated snapshots rather than live quotes. Page maintenance review: July 10, 2026. Verify current quotes and the latest official IR guidance before making a decision.

Disclosure: This article contains affiliate links to TradingView. We may earn a commission at no extra cost to you.

¥185 billion in operating income. A 42.3% operating margin. A record ¥505 dividend per share. Disco Corp. (6146) just posted its sixth consecutive period of record-high profit — and almost no US dividend investor is talking about the consumables revenue line that makes this payout structurally durable. — DividendDan

Investment Thesis

Author’s View: Constructive | Fair Value Estimate (Author’s Model): Thesis-based — 12-month re-rate contingent on FY2027 Q2 consumables revenue confirmation

- Near-monopoly in dicing saws and wafer grinders, plus a 30–35% recurring consumables revenue stream, converts every new AI chip fab order into a multi-year annuity — the record ¥505 dividend is the visible proof.

- FY2025 (Apr 2025–Mar 2026): net sales ¥436.9B (+11.1% YoY), operating income ¥185.0B, net income ¥135.5B; equity ratio 78.9%; payout ratio 25% base + performance-linked top-up.

- Top risk: FY2026 Q1 guidance (¥106.1B sales, ¥42.0B operating income) implies deceleration from a 21.1% five-year earnings growth average to ~9.4% YoY — demanding scrutiny at a 52x PER.

| Metric | Value |

|---|---|

| Price (JPY) | Y76,590 |

| Dividend Yield | 0.66% |

| P/E Ratio (TTM) | 61.5x |

| Market Cap | Y8.3t |

| 52-Week Range | Y37,260 – Y91,680 |

Disco Corporation (TSE: 6146) is not a household name among US dividend investors, but it probably should be. The company dominates a precision-processing niche sitting directly in the path of the AI capex supercycle. Full disclosure: see our Disclaimer — the author does not currently hold positions in securities discussed.

This article unpacks the full investment case: the macro tailwind, the business model moat, the dividend mechanics, and the risks that a 52x PER stock demands you take seriously.

What Disco Corp. Actually Does

Disco’s entire business is summarized in three Japanese verbs: kiru, kezuru, migaku — cut, grind, polish. The company manufactures dicing saws, laser saws, grinders, and polishers that process semiconductor wafers and electronic components after they leave the front-end fab.

Every time a wafer is diced into individual chips, a Disco blade is almost certainly involved. The company holds a dominant share in dicing saws and wafer grinders globally — a position built over decades of specialization that peers like Tokyo Electron (8035) and Advantest (6857) do not directly contest.

Critically for dividend investors, Disco also sells the consumable tools — dicing blades, grinding wheels, polishing pads — that wear out and must be replaced continuously. This consumables segment generates approximately 30–35% of total revenue and is far less cyclical than equipment sales.

FY2025 Earnings: Sixth Consecutive Record

Disco’s full-year results for FY2025 (April 2025 – March 2026), released April 22, 2026, were the sixth consecutive period of record-high profit. Key figures from the FY2025 earnings presentation:

- Net sales: ¥436.9 billion (+11.1% YoY)

- Operating income: ¥185.0 billion (operating margin: 42.3%)

- Net income: ¥135.5 billion (net margin: 31.0%)

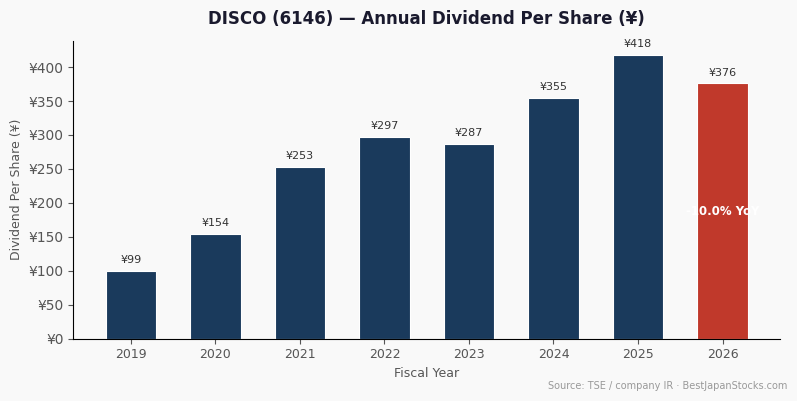

- Annual dividend per share: ¥505 (record)

The primary driver was sustained demand from generative AI infrastructure — hyperscalers and HBM (High Bandwidth Memory) suppliers ramping capacity at pace. Disco’s equipment sits at the back-end of that supply chain, processing the wafers that feed every AI accelerator.

For Q1 FY2026 (April–June 2026), Disco guided net sales of ¥106.1 billion and operating income of ¥42.0 billion. The company provides only one-quarter-ahead guidance due to market visibility constraints — a transparency limitation US investors should factor into their models.

The Dividend Mechanics: How ¥505 Is Built

Disco’s dividend policy has two layers. The base layer targets a 25% payout ratio of consolidated semi-annual net income.

The second layer is an additional distribution: if year-end cash reserves exceed a threshold after accounting for future investment needs, approximately one-third of the excess is paid out as a special dividend.

This structure means the ¥505 FY2025 dividend is not a static number — it scales with earnings and cash generation.

For US dividend investors accustomed to fixed quarterly payouts, this variable-plus-special structure requires a different mental model: think of it as a profit-sharing mechanism rather than a committed yield.

The equity ratio of 78.9% provides a substantial buffer. Even if earnings decline 20–30% in a cyclical downturn, Disco has the balance sheet strength to sustain meaningful dividend payments without taking on debt.

Japan-Local Intelligence: What US Analysts Miss

One data point that rarely appears in English-language research: Disco Corp. scores 3.88 out of 5.0 on OpenWork (Japan’s equivalent of Glassdoor), placing it in the top 1% of all Japanese companies.

Sub-scores include 4.6 for “Satisfaction with compensation” and 4.7 for “Compliance awareness.” The lower scores — 2.7 for “Long-term talent development” and 3.3 for “20s growth environment” — suggest a demanding culture focused on execution over mentorship.

For dividend investors, the high compliance and compensation scores are the relevant signal: they indicate a management team that pays fairly and operates within governance norms, reducing the risk of accounting surprises or labor disputes that could disrupt cash flow.

On Minkabu (みんかぶ) (as of May 24, 2026), the analyst consensus for Disco (6146) shows 10 “strongly constructive view” and 2 “Buy” ratings — 12 out of 12 analysts constructive — with an average fair-value estimate of ¥77,375, implying approximately 17.5% upside from the May 22 price of ¥65,860.

This unanimous domestic analyst consensus, combined with the OpenWork governance signal, reinforces the view that earnings quality is high and management credibility is intact — both prerequisites for dividend sustainability.

AI Capex Tailwind: How Long Does It Last?

The Japan Semiconductor Equipment Market is projected to reach USD 24.96 billion by 2033, driven by AI chips, advanced packaging, and HBM demand. Global semiconductor equipment sales are forecast to reach a record $139 billion in 2026, according to industry data.

New fab construction in Japan — including TSMC’s Kumamoto Phase 2 and Rapidus’s Hokkaido facility — creates a domestic demand pipeline for Disco’s equipment that extends well beyond the current AI cycle. Each new fab is a multi-year equipment order followed by decades of consumables replenishment.

For US investors tracking this via TradingView, Disco’s price action has closely tracked the Philadelphia Semiconductor Index (SOX) with a lag of roughly 2–4 weeks, making it a useful leading indicator for positioning.

Japan Edge: What Japanese Sources Add to the DISCO Thesis

DISCO is a global semiconductor-equipment name, but the Japan-specific edge is that investors can follow the company through unusually granular domestic disclosures before the full annual story is obvious.

The FY2025 financial results show shipment value of ¥442.824 billion, up 10.3% year over year, and net sales of ¥436.889 billion, up 11.1%. Operating income was ¥184.989 billion, with an operating margin of 42.3%. That margin profile is why DISCO should not be treated like a generic equipment maker;

it is a high-margin process-tool and precision-equipment cycle stock.

The same results explain the cycle mix in a way that many English summaries flatten. Demand from data centers, advanced logic, and HBM remained high, PC and smartphone demand showed gradual recovery, while power-semiconductor demand stayed weak due to the EV slowdown.

DISCO also said shipments of precision processing equipment for high-performance semiconductors remained strong and that precision processing tools stayed high because customer facility utilization was high. For a U.S. investor, the useful translation is this: do not monitor only headline semiconductor capex.

Track whether HBM/advanced logic strength and consumable tool demand are still offsetting weaker EV/power-semiconductor pockets.

| Local signal | Latest datapoint | Investor translation |

|---|---|---|

| Shipment value | FY2025 shipment value ¥442.824bn, +10.3% YoY | Use shipment value as a cycle indicator that can lead or clarify reported sales. |

| Margin durability | FY2025 operating margin 42.3%; ordinary income margin 42.3% | The valuation debate depends on whether high-value-added tools keep margins far above typical equipment peers. |

| Near-term guide | FY2026 1Q forecast: net sales ¥106.1bn, operating income ¥42.0bn, shipment value ¥132.0bn | Quarterly shipment guidance is the first item to compare against AI/HBM expectations. |

| FX assumption | FY2026 1Q forecast assumes USD/JPY of ¥157 | A stronger yen can pressure translated earnings; a weaker yen can flatter reported profit. |

| Dividend signal | FY2025 annual dividend ¥505; FY2026 dividend forecast not determined at the FY2025 release | Dividend income is real, but the primary thesis is cyclical growth and margins, not a stable high-yield profile. |

Local Watch Items for DISCO Investors

- Preliminary reports and quarterly shipment value: DISCO publishes preliminary and quarterly information on its IR site. These releases are worth checking before relying on delayed English commentary.

- HBM and advanced-logic mix: the FY2025 release directly links strength to data centers, advanced logic, and HBM. If those categories slow, DISCO’s premium margin story becomes harder to underwrite.

- Tools as a utilization proxy: precision processing tools are consumables. Strong tool demand can signal high customer fab utilization even when investors are worried about equipment-order timing.

- Yen sensitivity: compare each quarterly forecast’s exchange-rate assumption with the current USD/JPY rate. The FY2026 1Q assumption of ¥157 makes FX a visible part of the near-term model.

- Domestic sentiment check: use Japanese pages such as みんかぶ 6146 to see whether local investors are framing DISCO as an AI/HBM winner, an expensive momentum stock, or a cyclical peak-risk name.

The practical Japan Edge is not simply that DISCO is listed in Tokyo. It is that Japanese IR materials give investors a faster checklist: shipment value, application mix, tool utilization, yen assumptions, and dividend timing. If those signals stay aligned, DISCO can deserve a premium multiple.

If shipment value rolls over while the stock still prices in flawless AI/HBM demand, the risk/reward can change quickly.

Risks and Counter-View

A 52x PER is not a valuation that forgives disappointment. Here are three substantive counterpoints to the constructive thesis:

1. Earnings growth deceleration. Disco’s five-year earnings growth averaged 21.1% annually. FY2026 Q1 guidance implies approximately 9.4% YoY growth. If this deceleration persists, the current multiple is difficult to justify on a pure earnings-growth basis. Goldman Sachs removed Disco from its APAC Conviction List in April 2026 — a signal worth monitoring even if not definitive.

2. Semiconductor equipment cyclicality. Equipment spending is a leading indicator of fab capex, which itself is cyclical. A slowdown in AI infrastructure investment — whether from hyperscaler budget cuts, a macro recession, or a technology shift — would hit equipment orders before consumables, but consumables would follow.

The 30–35% recurring revenue stream dampens but does not eliminate cycle risk.

3. FX and geopolitical exposure. Disco sells globally but reports in yen. A strengthening yen compresses reported revenues from overseas sales. Additionally, US export controls on advanced semiconductor equipment to China represent a structural risk to a portion of Disco’s addressable market. The EDINET filings detail geographic revenue breakdown for investors who want to model China exposure precisely.

Bottom Line — Author’s View: Constructive with Conditions

Disco Corp. (6146) is a structurally sound business with a genuine competitive moat, exceptional margins (42.3% operating), and a dividend policy that has delivered six consecutive records. The ¥505 FY2025 payout is backed by real cash generation — not financial engineering.

The conditions on the constructive view: the 52x PER requires FY2027 consumables revenue to confirm that the recurring revenue stream is holding through the equipment cycle deceleration. If Q2 FY2027 consumables growth falls below 8% YoY, the valuation case weakens materially.

For a US dividend investor in the $500K–$2M portfolio range, Disco fits as a 2–4% position within a broader Japan technology allocation — not a yield play at 0.77–0.80%, but a total-return compounder where the dividend is the quality signal rather than the primary income source.

Data snapshot: May 2026; page maintenance review: July 10, 2026

Frequently Asked Questions

What is Disco Corp.’s current dividend yield and how is it calculated?

At ¥65,860 (May 22, 2026), the ¥505 annual dividend per share translates to approximately 0.77–0.80% yield. Disco’s policy combines a 25% base payout of semi-annual net income with an additional distribution of roughly one-third of surplus cash above investment thresholds.

The yield is low by US income standards, but the 42.3% operating margin and 78.9% equity ratio make it structurally durable.

What are the US tax implications of receiving Disco Corp. dividends?

Japan withholds tax on dividends paid to U.S. (non-resident) investors at a statutory rate of 15.315% (15% base rate + 0.315% reconstruction surtax).

U.S. individual investors holding portfolio positions may qualify for a reduced 10% treaty rate under the U.S.–Japan tax treaty (Article 10), but the lower rate applies only if your broker has collected the required treaty documentation (Form W-8BEN or equivalent); in practice, many retail investors receive the full 15.315% withheld at source.

The withheld amount is generally eligible for the foreign tax credit (IRS Form 1116) in taxable brokerage accounts; it is not recoverable in tax-advantaged accounts such as IRAs or 401(k)s.

Does Disco Corp. offer 株主優待 (shareholder perks)?

No. Disco explicitly does not offer 株主優待, prioritizing cash dividends as its primary shareholder return mechanism. This is actually advantageous for US investors, who typically cannot redeem Japanese shareholder perks anyway.

What are the main risks of investing in Disco Corp. at current valuations?

The three primary risks are: (1) valuation — a 52x PER leaves little margin for earnings misses; (2) cyclicality — semiconductor equipment demand can reverse quickly if AI capex slows; (3) FX — a stronger yen compresses overseas revenue in reported terms. China export control risk is an additional geopolitical overlay.

How to Buy 6146 from the U.S.

Disco Corporation (6146) trades on the Tokyo Stock Exchange Prime Market, with an OTC ADR also available under the ticker DSCSY. U.S. investors can access the stock through international brokers such as Interactive Brokers or Saxo Bank. For step-by-step brokerage setup, ADR vs. direct TSE shares, and U.S. tax handling, see our complete guide: How to Buy Japanese Stocks from the U.S..

Disclosure and Disclaimer: This article is for informational purposes only and does not constitute financial advice or a solicitation to buy or sell any security. Opinions are my own and not investment advice. The author does not currently hold positions in Disco Corporation (6146) or related securities at the time of publication.

Past performance is not indicative of future results. Always conduct your own due diligence before making investment decisions. In compliance with FTC 16 CFR Part 255, material connections are disclosed. See our full Disclaimer for complete disclosures. Data snapshot: May 2026; page maintenance review: July 10, 2026.

Primary Sources: Disco Corp. FY2025 Earnings Presentation (April 22, 2026) | Disco Corp. Basic Share Information (IR) | Disco Corp. IR News | EDINET FSA Filings | OpenWork — Disco Corp. Employee Reviews (3.88/5.0) | Minkabu (みんかぶ) — Disco Corp.

(6146) Analyst Consensus | Tokyo Electron IR (peer reference)