Educational research only, not investment advice. Market data changes frequently. See the full Disclaimer.

Data freshness: Market prices, yields, valuation multiples, and forecasts in this article are dated snapshots rather than live quotes. Page maintenance review: July 10, 2026. Verify current quotes and the latest official IR guidance before making a decision.

Disclosure: This article contains affiliate links to TradingView. We may earn a commission at no extra cost to you.

Hitachi’s decade-long transformation reached a new phase in April 2026. The April 2026 one-two punch — a Sovereign AI Factory alliance and an ¥800 billion shareholder return program in the same earnings cycle — finally made me stop treating this as a “wait and see” name. The Japanese-language medium-term management plan (中期経営計画) slides paint a Lumada margin trajectory that English-language wire coverage consistently undersells.

Investment Thesis | Data snapshot: May 2026; page maintenance review: July 10, 2026

Author’s View: Constructive | Fair Value Estimate (Author’s Model): ¥6,000 (12-month, thesis-based)

- Hitachi’s Sovereign AI Factory alliance and Lumada platform position it as the dominant Physical AI infrastructure vendor in APAC — a hardware-software-services stack with no direct Japanese peer.

- FY2025 revenue +8% YoY to ¥10.59 trillion; adjusted EBITA +21% to ¥1.31 trillion (all-time high); ¥500 billion buyback (3.56% of shares) plus ¥50/share annual dividend signals strong management conviction.

- Top risk: FY2027 net profit guidance came in below consensus, and a BOJ rate-hike path could strengthen the yen and compress overseas earnings.

| Metric | Value |

|---|---|

| Price (JPY) | Y4,615 |

| Dividend Yield | 1.18% |

| P/E Ratio (TTM) | 26.1x |

| Market Cap | Y20.8t |

| 52-Week Range | Y3,822 – Y6,039 |

Hitachi (TSE: 6501) has spent a decade shedding legacy businesses and rebuilding around digital infrastructure, energy transition, and AI-enabled industrial software. The FY2025 results announced April 27, 2026 confirm the transformation is generating real margin leverage — not just restructuring optics.

This article ties together the Lumada growth story, the Physical AI catalyst, and the ¥800 billion capital return program as a single, self-reinforcing thesis. Please review our Disclaimer before reading further.

Lumada: The Margin Engine US Investors Are Underpricing

Lumada is Hitachi’s proprietary digital platform that connects operational technology (OT) with IT across manufacturing, logistics, and infrastructure clients.

The platform generates recurring software and services revenue — a fundamentally different margin profile than the hardware-heavy Hitachi of 15 years ago.

Hitachi’s medium-term management plan (中期経営計画) (Mid-Term Management Plan, Japanese-language) explicitly targets Lumada revenue growth as the primary driver of EBITA margin expansion through FY2027.

English-language coverage tends to report Lumada as a product feature. The Japanese IR materials frame it as a platform ecosystem with compounding switching costs — a meaningfully different framing for valuation purposes.

For US investors tracking the stock on TradingView, the Lumada-driven margin inflection since FY2023 is visible in the earnings-per-share trend even before the FY2025 blowout.

Sovereign AI Factory Alliance: The Physical AI Catalyst

In April 2026, Hitachi announced a Sovereign AI Factory alliance positioning it as a key infrastructure vendor for national AI compute deployments across the Asia-Pacific region.

“Physical AI” refers to AI systems embedded in physical infrastructure — power grids, railways, water systems, manufacturing lines. This is distinct from cloud-native AI, and it plays directly to Hitachi’s OT heritage.

No direct Japanese peer competes across the full hardware-software-services stack that Hitachi offers in this space. That is a genuine competitive moat, not marketing language.

The alliance also aligns with Japan’s national AI strategy and METI energy policy reforms, giving Hitachi a quasi-policy tailwind that is difficult for foreign competitors to replicate quickly.

Green Energy & Mobility: The Structural Demand Story

Hitachi’s Green Energy & Mobility segment posted strong growth in FY2025, driven by grid equipment demand and railway system orders.

Japan’s energy transition — accelerated by METI’s energy policy reforms — requires massive grid modernization investment. Hitachi is a primary domestic supplier of high-voltage equipment and smart grid systems.

Railway systems are similarly structural. Japan’s rail operators are in a multi-decade upgrade cycle, and Hitachi’s signaling and rolling stock divisions are well-positioned to capture that spend.

For US investors, this segment provides a degree of domestic Japan revenue that is naturally hedged against yen weakness — a useful offset to the overseas earnings FX exposure.

Capital Return Program: ¥800 Billion in Shareholder Conviction

The ¥800 billion shareholder return program announced alongside FY2025 results consists of two components.

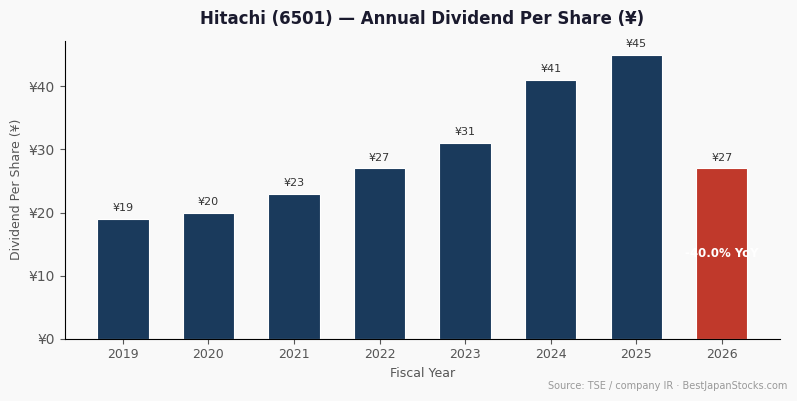

First, a ¥500 billion share buyback that will retire approximately 3.56% of shares outstanding. This is mechanically accretive to earnings per share even if net income stays flat.

Second, a ¥50 per share annual dividend. At the current price of approximately ¥4,770, this translates to roughly 1.0% yield — modest in absolute terms, but the buyback component adds meaningful total return on top.

Management’s willingness to commit ¥800 billion — against a market cap of ¥21.5 trillion — signals high internal conviction in the FY2026-2027 cash generation outlook. The EDINET filing (Japanese) provides the full legal disclosure of the buyback terms.

Japan Edge: What Japanese Employees and Retail Investors Are Saying

One data point US investors cannot easily access: Hitachi’s employee satisfaction rating on OpenWork (openwork.jp) sits at approximately 3.5 out of 5.

That is above the Japanese corporate average and suggests the internal culture has evolved alongside the external transformation narrative. Management quality proxies matter for long-duration thesis integrity.

On Minkabu (みんかぶ), Japanese retail investor sentiment on 6501 has been cautiously constructive post-earnings, with commentary noting the FY2027 guidance miss as a near-term overhang but broadly endorsing the Lumada trajectory. This is retail sentiment that English-language sources simply do not capture.

Risks and Counter-View

The thesis is not without meaningful risks. US investors should weigh at least three counterpoints before sizing a position.

1. FY2027 guidance miss. Hitachi’s net profit guidance for FY2027 came in below analyst consensus. If Lumada growth decelerates or integration costs from recent acquisitions prove stickier than expected, the premium valuation (27x P/E, 3.7x P/B) is vulnerable to de-rating.

2. BOJ rate hike path. The Bank of Japan’s April 28, 2026 policy meeting showed a 6-3 hawkish vote split, per BOJ 主な意見 (Summary of Opinions). A faster-than-expected yen appreciation cycle would compress Hitachi’s overseas earnings when translated back to JPY — the opposite of the tailwind enjoyed during the weak-yen era.

3. Execution risk on Physical AI. The Sovereign AI Factory alliance is strategically compelling but early-stage. Revenue recognition timelines for large government infrastructure contracts are notoriously unpredictable. The market may be pricing in a smoother ramp than is realistic.

Bottom Line — Author’s View: Constructive on 6501

Hitachi at ¥4,770 is not a deep-value dividend play — the 1.0% yield alone will not move the needle for income-focused US investors. The thesis is total return: a 21% EBITA growth engine, a 3.56% share count reduction, and a Physical AI moat being built in plain sight.

The P/E of 27x and P/B of 3.7x demand continued execution. The FY2027 guidance miss is a legitimate near-term concern. But for a US investor seeking Japan exposure with genuine earnings momentum and a credible management capital-allocation track record, 6501 earns a constructive stance at current levels.

Fair Value Estimate (Author’s Model, 12-month horizon): ¥6,000, assuming Lumada margin expansion continues and BOJ rate hikes remain gradual rather than aggressive. That implies approximately 26% upside from the ¥4,770 reference price — with the buyback providing a floor mechanism as shares decline.

Frequently Asked Questions

What is Hitachi’s current dividend yield for US investors?

Hitachi pays ¥50 per share annually. At approximately ¥4,770 per share, that is roughly 1.0% in yen terms. After the 15.315% Japanese withholding tax under the US-Japan tax treaty, the net yield to a US investor is approximately 0.85% — modest, but the ¥500 billion buyback adds meaningful total return on top.

Does Hitachi offer 株主優待 (shareholder perks)?

Hitachi does not operate a formal 株主優待 program as of the most recent IR filings. The capital return is concentrated in the dividend and buyback structure, which is more accessible to overseas investors than product-based perks would be.

How does the BOJ rate hike risk affect Hitachi specifically?

Hitachi generates a significant share of revenue outside Japan. A stronger yen reduces the JPY value of those overseas earnings when consolidated. The April 28, 2026 BOJ meeting showed a 6-3 hawkish split — a faster rate-hike path than expected would be a headwind to FY2026 earnings translations.

Can I hold Hitachi (6501) in a US IRA or 401(k)?

Yes, you can hold TSE-listed stocks in a self-directed IRA through brokers like Interactive Brokers. However, Japanese withholding tax on dividends paid into an IRA is generally not recoverable via Form 1116 (which requires taxable income). Consult a tax professional before placing Japanese dividend stocks inside a retirement account.

How to Buy 6501 from the U.S.

Hitachi (6501) trades on the Tokyo Stock Exchange, and since there is no actively traded U.S. ADR with meaningful liquidity, direct TSE access is the practical route for most U.S. investors. For step-by-step brokerage setup, ADR vs. direct TSE shares, and U.S. tax handling, see our complete guide: How to Buy Japanese Stocks from the U.S..

Related Articles

- How U.S. Investors Can Buy Fanuc (6954) at +15.5% Earnings Growth

- How U.S. Investors Can Buy Buffett’s Mitsui (8031) at 3.5% Yield

- How U.S. Investors Can Capture Disco Corp. (6146) ¥505 Dividend

- How U.S. Investors Can Buy KDDI (9433) at 3%+ Yield in 2026

- Mitsubishi Corp (8058): The 2026 Hub Analysis for Trading Houses

Key Primary Sources: Hitachi earnings report (決算短信) (Japanese IR) | Hitachi medium-term management plan (中期経営計画) (Japanese) | EDINET (Japanese FSA filings) | BOJ 主な意見 (Japanese) | OpenWork 6501 Employee Reviews (Japanese) | Minkabu (みんかぶ) 6501 (Japanese retail sentiment) | METI Energy Policy (English)

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Opinions are my own. Current position information is not provided for this article; do not infer a holding from the thesis. This content is subject to FTC 16 CFR Part 255 disclosure requirements. Always conduct your own due diligence before making investment decisions. Data snapshot: May 2026; page maintenance review: July 10, 2026.

Note for US tax purposes: Japanese dividend withholding is 15.315% (Japan’s statutory withholding; the U.S.–Japan treaty rate is 10% where properly documented). Claim the foreign tax credit on IRS Form 1116 if holding in a taxable account. Do not assume the credit is available inside an IRA — consult a tax professional.